If you’re invoicing US clients from Ghana, you already know the math doesn’t add up.

Platform fees take 1%. Currency conversion takes another 3%. Correspondent banks take $35–50 off the top before your bank even sees the wire. By the time cedis land in your account, you’ve lost 6–8% of your invoice. And you’ve waited up to 5 business days to use your own money.

You’re not doing anything wrong. The tools weren’t built for professionals running a small business across borders.

So here’s where the money actually goes — and what’s finally starting to work for Ghanaian freelancers and tech vendors in 2026.

You’ve probably tried them all. International wires. Payment platforms. Newer fintech wallets.

They all have the same three problems:

And the most popular payment apps US clients love to use? They don’t even work for local Ghana accounts.

Over a year of steady invoicing, those hidden costs add up to thousands of dollars. Gone.

Let’s break it down.

Platform fees. Take Upwork and Fiverr, the two most common platforms for Ghanaian freelancers:

Add currency conversion, withdrawal fees, and annual charges on top of that, and you’re well past 10% before the money even reaches Ghana.

Correspondent banks. Here’s the part nobody puts on a fee schedule. When your US client sends a wire, the money doesn’t travel directly. It hops through a chain of banks. Each one takes a cut — usually $35–50, plus a hidden FX markup. Settlement takes up to 5 business days. Longer if any bank in the chain flags the payment for review.

The experience is always the same. Your client says “I sent $1,000.” Your bank shows $940 five days later. Nobody can tell you where the missing $60 went.

This is the invisible tax on cross-border payments. And it’s the reason every serious fintech is trying to bypass correspondent banking entirely.

A newer generation of fintechs looks like progress. Fees are lower. Onboarding is faster. They understand the freelancer use case.

But they all make the same choice: your money lands in their wallet first. You have to log in, convert it, and withdraw it yourself.

That creates four problems you might not have noticed.

They earn the interest — not you. Every day your USD sits in a provider’s wallet, they earn yield on your float. You earn nothing. Move the same money to your own bank account and it works for you instead.

You carry the FX timing risk. Cedi–dollar rates move. A lot. Funds parked in USD waiting for you to manually convert expose you to volatility you never asked for.

Compliance freezes happen more than you’d think. Wallet providers periodically pause withdrawals during fraud reviews or platform upgrades. Your working capital can be stuck for weeks.

It’s an extra step every single time. Log in. Convert. Select a bank. Initiate the withdrawal. Wait. Multiply that by every invoice, every month.

The wallet model is a workaround for broken banking rails — not a replacement for them.

Here’s what getting paid looks like today — and what it looks like with a direct-to-bank rail like Instarails.

When payments land directly in your bank account — as cedis, in minutes — a few things change right away.

Your cash works harder. Money in your own bank earns interest. Money in a provider’s wallet earns interest for them.

You pay suppliers on time. Hotels, guides, contractors, developers — they don’t wait three days for SWIFT to clear. Now you don’t have to make them.

Your FX rate is predictable. Transparent conversion. No markup buried in the rate. You know exactly what lands before the money moves.

Your total cost drops to under 1.5%. No stacking platform fees, correspondent fees, and FX skim on top of each other.

You never touch a wallet. No conversions. No manual withdrawals. No waiting.

“What sold me on Instarails is that I don’t deal with a wallet at all. My US clients send payment and it lands directly in my Fidelity Bank Ghana account as cedis — instantly, at the best FX rate I’ve seen. Before, I was losing over 5% to fees and waiting days for SWIFT to clear before I could pay hotels, guides, and drivers. Now the money arrives in minutes, ready to use — and because it sits in my bank, not a wallet, it’s actually earning interest. It’s changed how efficiently I run my travel business.”

— Nana Afriyie Mensah-Boadu, Cosmopolitan Travel Services, Accra, Ghana

Cosmopolitan Travel Services now gets paid same-day, in cedis, directly to its Fidelity Bank account. Working capital is available when it’s needed — not three days later. And the money starts earning deposit interest immediately, before a single supplier invoice goes out.

The best option depends on where your payments come from.

If you earn through freelance marketplaces (Upwork, Fiverr), use Instarails for payments and save 10–20%.

If clients pay you directly — invoicing, retainers, service contracts, tour bookings, vendor payments — a direct-to-bank rail will almost always be cheaper and faster. This is where the 5%+ savings compound into real money.

For most Ghanaian SMEs, freelancers, and tech vendors, direct-to-bank settlement is the meaningful upgrade. It removes the wallet step, the correspondent-bank tax, and the FX opacity in one move.

Instarails delivers US payments directly into your Ghanaian bank account as cedis — in minutes, at a low, transparent rate, with no wallet in the middle. We also pay into MTN Mobile Money, Vodafone Cash, and AirtelTigo for recipients who prefer mobile wallets.

A standard international wire transfer takes up to 5 business days. Sometimes longer if a correspondent bank flags the payment for review. Direct-to-bank payment rails that bypass correspondent banking can settle in under 60 seconds.

Instarails settles directly into major Ghanaian bank accounts. We also pay into MTN Mobile Money, Vodafone Cash, and AirtelTigo mobile wallets. Check with us to confirm your specific bank.

The complaints are remarkably consistent across every corridor. On r/ghana, Ghanaian remote workers regularly post variations of “I just got hired, they want my PayPal, and I know PayPal doesn’t work here” — and the top replies cycle through Payoneer, Wise (with a foreign currency account workaround), and bank transfers, each with their own fee and delay problems. One Ghanaian commenter even noted that Wise suspended remittance to Ghana on their platform, pushing users toward foreign currency accounts.

Zoom out to the broader freelancer community and the pattern repeats. On r/digitalnomad, one thread breaks down the true cost of common options: Wise at 0.4–1.5% variable fees depending on corridor, PayPal at 5% international fee plus 2.5–3% FX spread, Revolut with monthly limits and occasional account freezes. On r/smallbusiness, a business owner paying freelancers in five countries wrote that “PayPal and bank transfers work, but the fees and rates eat a lot. I’m looking for ways to pay people in their local currency without hidden costs.” Another commenter on the same thread: “Hidden costs are real. I thought I was paying 1% until I compared mid-market rate vs what actually arrived. Some corridors were 4-5% worse.” Similar pain surfaces on r/Entrepreneur, where entrepreneurs trade workarounds for accepting foreign payments that don’t bleed them on fees.

The question everyone is really asking: why isn’t there one app that just delivers local currency directly, at a transparent rate, without a wallet in the middle? That’s the gap Instarails was built to fill.

Yes — through a foreign currency account at most major Ghanaian banks. But USD sitting in a foreign currency account still has to be converted to cedis for local spending. And the bank’s conversion rate is often 1.5–3% worse than the mid-market rate. Direct-to-bank GHS settlement avoids this step entirely.

April 18, 2026

Struggling to Get Paid in Ghana? Here’s Why — and What Works

From startups to enterprises, businesses trust Instarails to move money across borders — instantly and affordably.

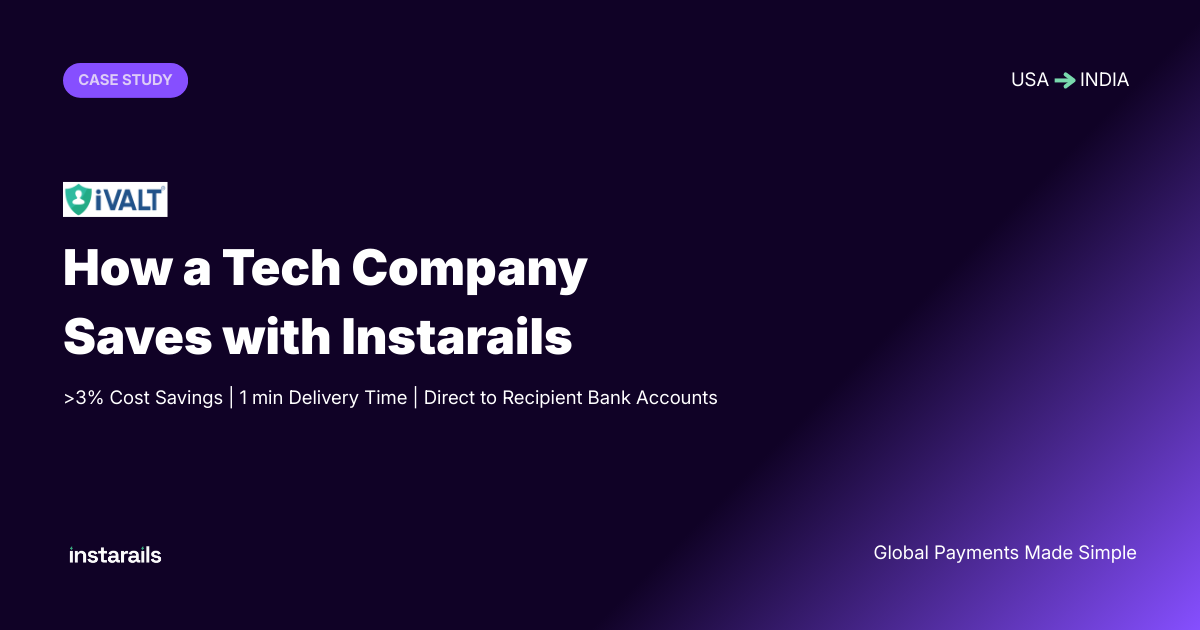

"Switching to Instarails for invoicing our U.S. clients was a game-changer. We used to get poor FX and on top of that, bank charges were eating into every payment. It was silently adding up to around 15% loss on every transfer. Now with Instarails, we get the live exchange rate, zero surprises on charges, and the money hits our account in under 30 minutes. It's faster, cheaper, and honestly just simpler. Highly recommend Instarails to any tech company in India billing U.S. clients."

" Instarails has transformed how we handle international payments. Their platform saves us at least 3% in costs, directly improving our bottom line. The batch upload feature streamlines our processes, but what's most impressive is the impact on our overseas team — they now receive their full salaries directly in their bank accounts in under one minute, with zero deductions."

"We recently ran into an issue where both of our overseas payment platforms went down at the same time, and we needed a fast solution to pay our global team. The setup with Instarails was simple, smooth, and the payments were lightning fast. Huge relief on our end. Definitely recommend Instarails to any employer looking for a reliable way to pay international team members without the headaches."

"What sold me on Instarails is that I don't deal with a wallet at all. My US clients send payment and it arrives directly in my Fidelity Bank Ghana account as GHS — instantly, at the best FX rate I've seen. Before, I was waiting days for SWIFT transfers to clear and losing over 5% to fees and poor conversion rates. Now the money arrives in minutes, ready to use — and because it's sitting in my bank account, not a wallet, I'm actually earning interest on it. It's changed how efficiently I run my travel business."

"Instarails onboarded us in five minutes. Our US clients pay us and the money lands in our bank account almost instantly. The fees are a fraction of what we used to pay, and we get market exchange rates. No more waiting days or losing money to mystery charges. It's the easiest way we've ever gotten paid."

"As a freelancer working with U.S. clients, I used to dread payment day. Between bank wire fees and terrible exchange rates, I was losing approximately 3% on every invoice. On a $10,000 project, that's $300 — almost ₹25,000 — just vanishing. Since I started using Instarails, everything changed. I send my invoice, my client pays, and the money hits my account instantly at the best FX rate with the lowest fees. Plus, I get a proper invoice for my records. "